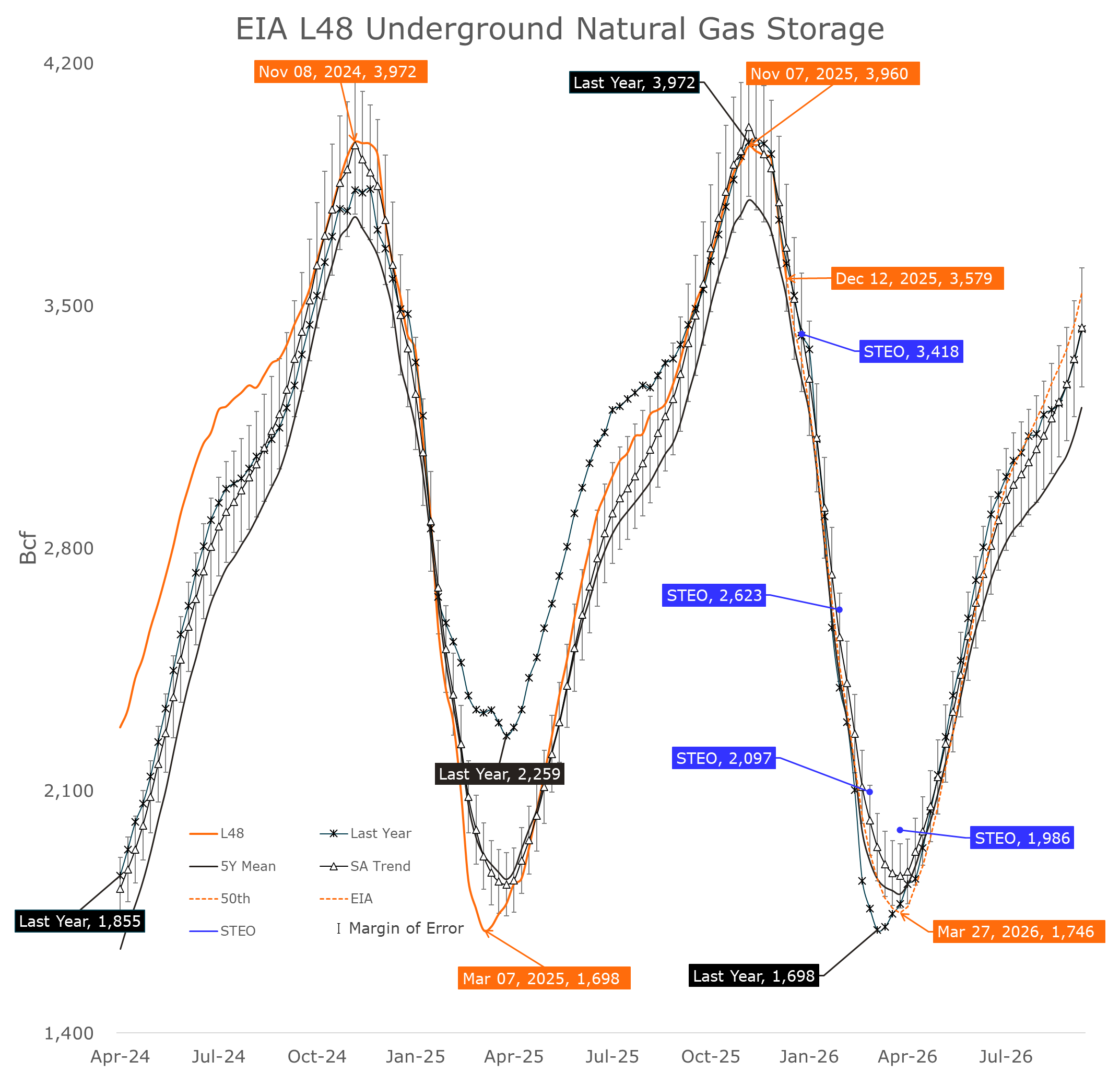

As anticipated after last week’s weather, the EIA printed another outsized storage withdrawal. For the week ending December 12th, working gas fell by 167 Bcf, pulling inventories down to 3.579 Tcf. That ranks among the largest early season pulls of the past decade versus a typical move this time of year of roughly 127 ± 19 Bcf.

As of last Friday, December 12th, L48 natural gas storage stood at 3.579 Tcf as one of weakest starts to winter quickly morphed into one of the strongest starts. By our estimates, inventories are on pace to end winter with around 1.746 Tcf in ground… well below the EIA’s aggressive estimate of 1.986 Tcf. We shall see.

With this report, cumulative withdrawals for the season are 381 Bcf, a notable pivot from an early start that initially looked soft. Near-term, the next EIA print will be heavy, but likely below the last two releases—early estimates span the low-120s to low-160s Bcf. Beyond that, withdrawals will moderate as Midwest and Mid-Atlantic temperatures are forecast to trend toward near- to above-normal. It’s still early winter, and forecast error/variance remains high. On current inputs, our end-of-season inventory projection stands at ≈1.747 Tcf, with a wide error band of ±114 Bcf.

The last two massive deliveries pushed this season’s hitherto withdrawal from one of the weakest to start a season, to one of the strongest to start a season.

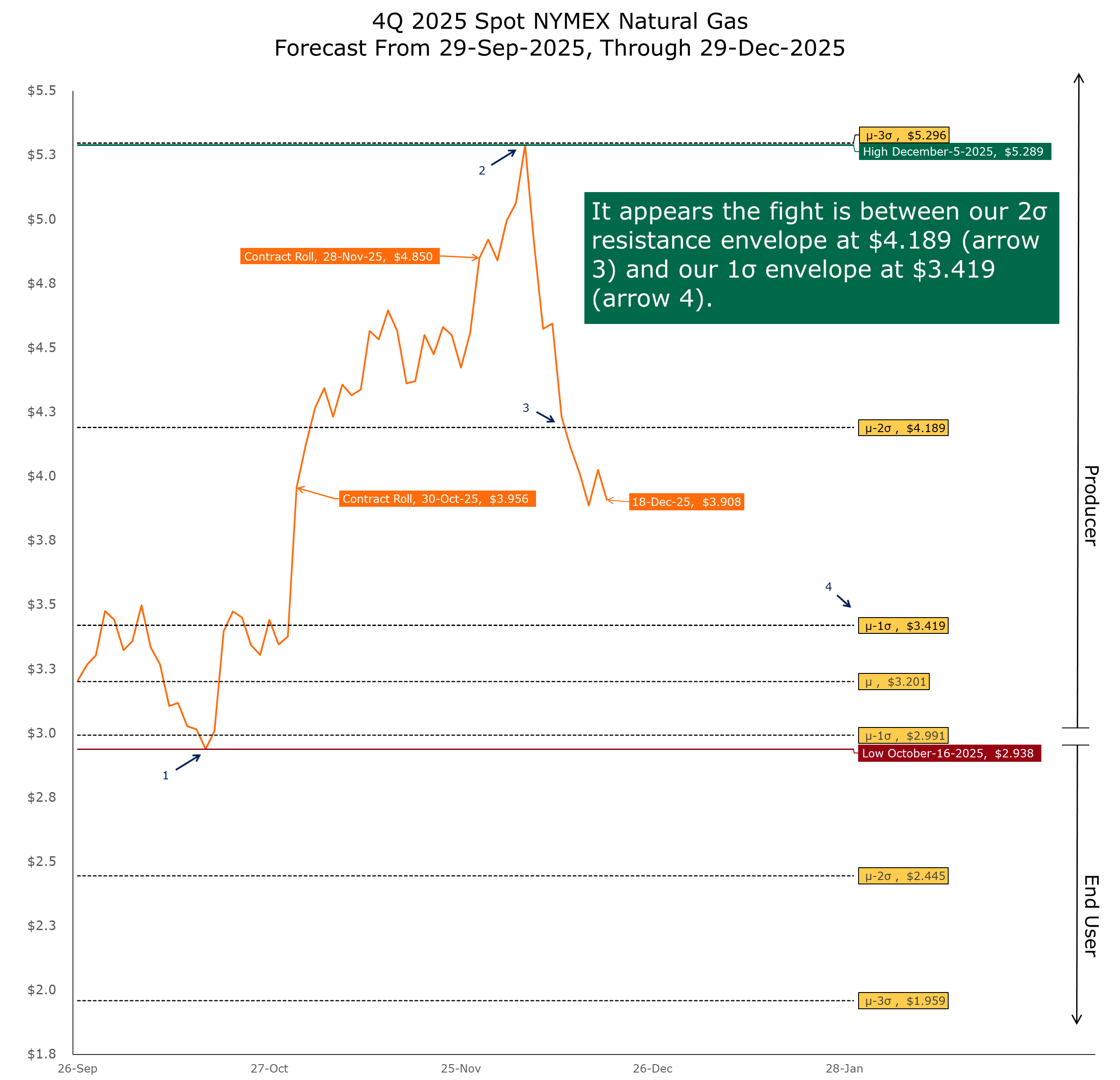

The Henry Hub complex is giving a master class on what a weather-premium unwind looks like. On December 05th, Jan-26 gas hit an eight-month high at $5.496, which was the highest high for spot gas in three years. Ten days later, traders were staring at a vastly different market: this past Tuesday, the contract bottomed at $3.842 and settled at $3.886, the lowest prints since the end of the 2021–22 winter. The following session delivered a profit-taking bounce, but yesterday’s EIA release brought the bears back in, and the market finished at $3.908.

The NYMEX term structure confirms the message that traders are shifting out of winter and moving further down the curve. The Feb-26 through Apr-26 markets have fallen harder than the spot Jan-26 contract. Most importantly, the cross-seasonal Mar/Apr backwardation—the market’s winter-to-shoulder truth serum—narrowed to nine-tenths of a cent. That’s not a spread; it’s a rounding error. In plain English, the market is no longer paying a meaningful premium to own late-winter exposure versus the shoulder season.

Our Q4 2025 seasonal model captures the anatomy of the rise and fall. The market’s October low at $2.938 (arrow 1) dipped $0.053 below the model’s first standard-deviation floor at $2.991—an exhaustion print. Then December delivered the other tail: the December 05th high close at $5.289 (arrow 2) finished within seven-tenths of a cent of the third standard-deviation ceiling at $5.296. That’s a full-range regime swing—about as clean as you’ll ever see.

Throughout this quarter, we have been treated to full-range price swing from below our models 1σ floor at $2.991 to within a whisker of the 3σ ceiling at $5.296, surging through the 2σ ceiling at $4.189. According to the latest read from the options, odds are 10 to 1 (9.4% probability) we will see a break below the 1σ ceiling of $3.419 and 7 to 2 odds

(22.3% probability) of a rebound above $4.189.

From there, gravity took over and the market is now trading below the second standard-deviation ceiling at $4.189 (arrow 3). With ten days to go before the Jan-26 expiration, the fight is between the second standard deviation ceiling and the first standard deviation ceiling of $3.419 (arrow 4).

As of yesterday’s settlement, the options market implied volatility (IV) on the $3.40 put strike of 68.69% indicates a 9.4% probability (odds of 10 to 1) the market will break support at $3.419. The IV on the $4.200 call strike of 68.33% indicates a 22.3% probability (7 to 2 odds) of a rebound above $4.189.

The Schork Group has established a niche as the benchmark for objective insight—delivering energy market intelligence through a neutral lens. In today’s data-saturated environment, markets are noisy—and readers rely on us to cut through the clutter, identify what truly moves prices, and deliver direct signals to manage risk. Learn more about our products and services: www.schorkgroup.com.